Solar Financing In 2026: Exploring Solar PPA, PrePaid PPA, and Cash Options

The solar energy landscape in California has undergone a seismic shift. With the full implementation of Net Energy Metering 3.0 (NEM 3.0) and the expiration of the long-standing federal residential solar tax credit at the end of 2025, homeowners considering solar power in 2026 face a new set of economic calculations.

The Power Purchase Agreement (PPA) is still a prominent financing option, offering an alternative path to solar adoption and has also changed to adapt to the current landscape. This guide provides a comprehensive analysis of solar PPA options in California for 2026, examining the current policies, financial implications, and the pros and cons of PPAs.

By covering this topic in depth, we aim to empower homeowners with the understanding of their financing options for solar.

The 2026 California Solar Landscape: NEM 3.0 and Expired Tax Credits

Two major policy changes have fundamentally altered the financial equation for residential solar in California. Many homeowners are still wondering if solar is worth it in the long run. Let’s break down what the changes were, and how that impacts the financial equation over the long-haul.

The Expired Residential Tax Credit: What It Means for Upfront Costs

The second major change is the expiration of the federal Residential Clean Energy Credit (under Section 25D of the tax code) for homeowners. According to the IRS, this 30% tax credit is not available for residential homeowners after December 31, 2025.

This means that a homeowner who purchases a solar system in 2026 cannot claim the 30% federal tax credit, which increases the upfront cost and extends the payback period. However, as a Lifetime Energy Partner for thousands of homeowners, we’ve found a way to get you the equivalent of those expired tax credit savings, and apply those savings directly to the cost of solar. It’s a win-win for homeowners who want to maximize their lifetime energy cost savings!

Your Three Paths to Going Solar in 2026

The financial equation for solar has shifted, but the goal remains the same: achieving energy independence and long-term savings. Here are the three main solar financing paths available to you in 2026.

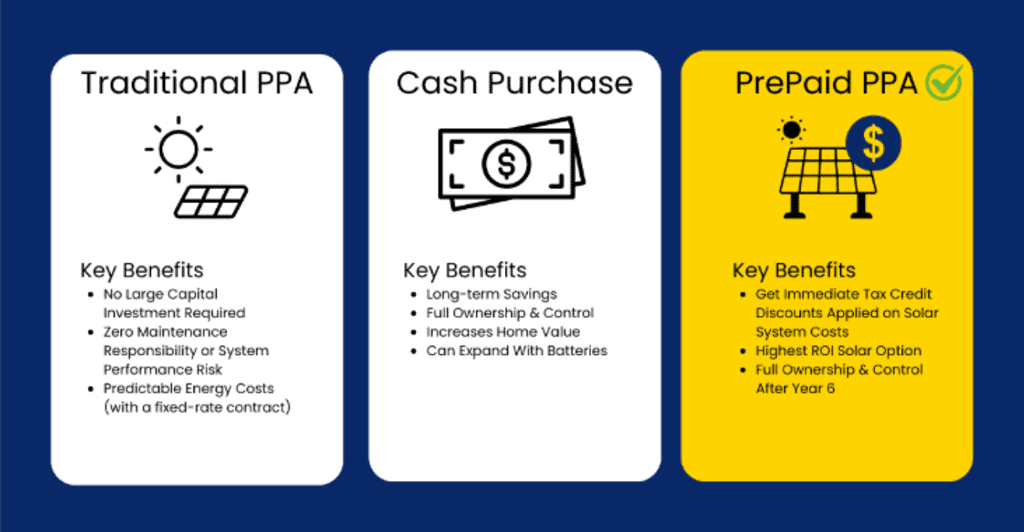

Option 1: Buying the System Outright

The outright solar purchase is the traditional standard for maximizing savings. You purchase the solar system with cash or solar loans, and you own it from day one.

- Pros: Long-term savings, it increases home value, and gives homeowners full control over systems.

- Cons in 2026: The 30% federal residential tax credit is no longer available, making the upfront cost significantly higher. The payback period would become even longer than a typical NEM 3.0 system with federal tax credits.

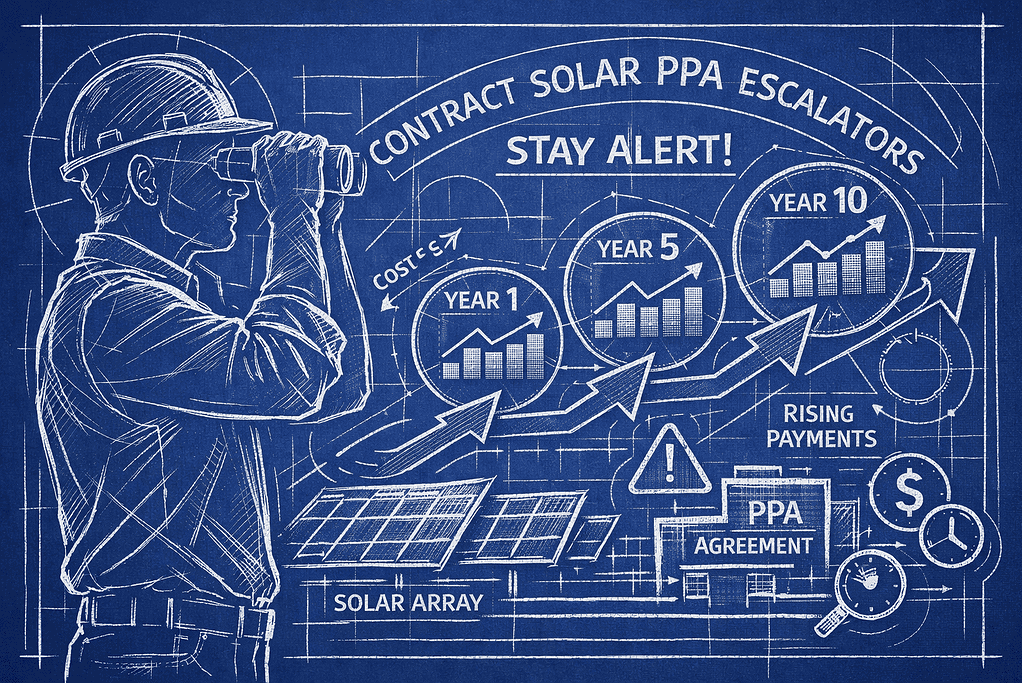

Option 2: The Traditional PPA

This is the classic “go solar for $0 down” model. A solar company installs and owns the panels on your roof, and you agree to buy the power it produces for the next 20-25 years at a set rate or with escalating rates defined in your contract.

- Pros: No upfront cost, predictable energy rates (with a fixed-rate contract), no maintenance responsibility.

- Cons in 2026: You don’t own the system and see the lowest long-term savings. It can severely complicate selling your home, and you can still receive surprisingly high true-up bills from your utility.

Option 3: The Modern Solution - The Prepaid PPA

This model has been adapted for the 2026 landscape and represents the best of both worlds. It is designed to give homeowners the benefits of ownership while leveraging incentives that are no longer available to them directly. While the residential tax credit has expired, the commercial tax credit has not. Given the change in solar tax credits in 2025, this is the recommended solar option until the end of 2027 – with the highest cost-savings. When paying for a system with cash and using a prepaid PPA, typical payback periods can range from 5-7 years.

Our Founder Chris Moran Speaking About Solar Options in 2026:

Why the Prepaid PPA is the Smart Choice for 2026

What’s Different For PPAs in 2026

While the residential tax credit has expired, the commercial tax credit (under Section 48E) remains available. PPA providers, as commercial entities, can claim this credit and pass the savings on to homeowners in the form of lower electricity rates. PrePaid PPAs are one of the best ways for homeowners in 2026 to indirectly benefit from a federal solar incentive.

How Traditional PPAs Operated

A PPA is a financial agreement where a solar developer designs, permits, finances, and installs a solar energy system on a customer’s property at little to no cost. The customer then agrees to purchase the power generated by the system from the developer for a fixed term, typically 20 to 25 years. The PPA provider retained ownership of the system and any associated tax credits or incentives, while the customer benefited from predictable energy pricing and reduced utility bills without system ownership.

Complications With The Traditional Solar PPA

Many homeowners were attracted by the promise of “$0 down solar”, but these deals often came with long-term contracts that created unexpected financial challenges.

Key Issues:

25-Year Contracts with Escalators:

- The initial low electricity rate can increase annually.

- This escalation compounds and can erode long-term savings.

Complications When Selling Your Home:

- Prospective buyers are often reluctant to assume a decades-long solar contract.

- Sellers face tough choices: Pay a large buyout fee to terminate the contract, or risk losing the sale entirely.

The Closing Window: Why You Must Act Now to Secure Your Savings

This opportunity is built upon the Commercial Investment Tax Credit (Section 48E), which allows businesses and tax-exempt organizations to claim up to 30% of the cost of qualifying zero-emission electricity generation and energy storage facilities, and will end on December 31, 2027*.

(*Dates around laws are subject to change.)

Waiting is no longer a viable strategy. The process of designing a system, securing financing, and completing the necessary paperwork to meet the “begin construction” deadline takes time.

Don’t wait too long otherwise you’ll miss out!

Conclusion and Recommendations

Navigating the solar landscape in 2026 requires a new strategy. Don’t worry, Solar Negotiators is here to break the information down so you can understand all the recommended options to go solar in 2026.

While the expiration of the residential tax credit has made traditional system purchases more expensive, the Prepaid PPA has emerged as a powerful alternative. If you thought you missed the federal tax credits, well think again!

It uniquely combines the long-term financial benefits of ownership with a significant upfront discount made possible by the commercial tax credit. For California homeowners looking to maximize their savings and secure true energy independence, the Prepaid PPA represents the most intelligent and financially sound path forward.

Disclaimer: The information provided regarding the federal solar tax credit is for general informational purposes only and should not be construed as legal, financial, or tax advice. Eligibility for the solar tax credit may vary based on individual circumstances, including income level, tax liability, property ownership, and system installation details. Tax laws and incentives are subject to change and may differ by jurisdiction.

We strongly encourage all homeowners to consult with a qualified tax professional or financial advisor to determine how the solar tax credit may apply to their specific situation. Only a licensed expert can provide guidance tailored to your unique financial profile and ensure compliance with current IRS regulations.

FAQs

What happens if the solar company goes out of business during the 5-6 year “safe harbor” period of a Prepaid PPA?

This is a critical question that highlights the importance of choosing a reputable, well-established solar partner. In a properly structured Prepaid PPA, your agreement is with the financing entity that partners with the solar installer, and your prepayment is secured. The ownership transfer is a legal requirement of the contract. Furthermore, the physical assets—the panels and equipment on your roof—are part of the agreement and cannot simply be removed. Reputable companies will also have provisions for transferring maintenance and monitoring obligations to another certified installer in the event they cease operations, ensuring your system continues to be supported. It is always important to discuss these terms with your provider before signing a contract.

Is a battery system required with a Prepaid PPA under NEM 3.0?

While not technically required by the financing structure itself, a battery system is considered practically essential for maximizing your savings under NEM 3.0. Forgoing a battery means you will lose valuable electricity your system generates while the sun is out and need to buy expensive power from your utility every night, significantly undermining the financial benefits of your solar investment.

Is a PrePaid PPA better than a cash purchase in 2026?

For the vast majority of homeowners in 2026, yes, a Prepaid PPA is financially superior to a straight cash purchase. Here’s the simple math: with the 30% residential solar tax credit (Section 25D) now expired, a cash purchase requires you to pay 100% of the system’s cost out of pocket. A Prepaid PPA, however, leverages the commercial tax credit (Section 48E) to give you an upfront discount of approximately 30%.

If I sign a Solar PPA in 2026, can I eventually own the panels?

This depends entirely on which type of PPA you sign.

- If you sign a Traditional PPA, the answer is no. You are only paying for the electricity the system generates for a 20-25 year term. At the end of the contract, you do not own the panels. Your options are typically to renew the PPA, have the system removed, or purchase the system at its Fair Market Value at that time, which could still be a significant cost.

- If you sign a Prepaid PPA, the answer is yes. This model is specifically designed as a financing path to ownership. After the 5-6 year safe harbor period required for the commercial entity to claim the tax credit, full legal ownership of the panels and all equipment automatically transfers to you at little to no cost. This is the fundamental purpose and benefit of the Prepaid PPA structure.

How is a Prepaid PPA different from a traditional solar lease?

A traditional solar lease is like renting an apartment; you make fixed monthly payments for 20-25 years to use the system, but you never build equity and do not own it at the end. A Prepaid PPA is more like a temporary agreement; you make one large upfront payment (at a significant discount) and, after a set period of 6 years, you take back full ownership of the system. The key difference is the end result: a lease offers temporary use, while a Prepaid PPA is a direct path to ownership and long-term asset value.

Recent Posts

High Solar Bills Explained: Why Your True-Up or PPA is Costing More Than Expected

Solar Financing In 2026: Exploring Solar PPA, PrePaid PPA, and Cash Options

What Happens After the Solar Tax Credit Ends in 2025?

Reduce your reliance on the energy grid.

Get Solar In

Your Inbox

Refer friends and get paid in-app

The more referrals you bring in, the higher your earnings.

Earn $1,000 for each referral, and bonuses of up to $1,500 once you hit your 10th referral.